Weather is one of those things that we all talk about….daily. It’s one of the worlds most common used “ice-breakers.” Speaking of ice breaking, hail can come in a hurry and do a whole lot of breaking. Whether (weather?) the damage occurs to your vehicle, house, garden or field, you should carry hail insurance on your property.

Where can I insure my crops?

While you can insure your crops for certain perils such as: Flood, Fire or Drought with Saskatchewan Crop Insurance, and you can purchase Hail Insurance coverage through our office or your local municipal office. We have 2 major carriers: Coop Hail Insurance & Palliser Insurance. Both companies are extremely reliable, with competent adjusters and great customer service.

How do I insure my crops?

When you come in to our office to insure your crops, you will need to know your land locations that these crops are located on. We will need to know the type of crops, and the number of acres that was seeded on each location and the value you want to insure per acre ($100/acre).

With that information, we are able to calculate a rate for your hail insurance. Each crop can withstand hail differently, so the rate can fluctuate based on the type of crop. For example, Lentils may have a rate of 1.75 x Basic Rate. Each company may vary on these surcharges, so it’s important to talk to a broker on which company offers the best products for your crop.

When does my policy become effective and for how long?

When a Hail Insurance policy is purchased, the policy becomes effective at 12PM (Noon) the following day. Most companies stop offering hail insurance coverage around August 15th. That deadline may come sooner if the insurance company has met their capacity. Policies expire on October 15th or when the crop is harvested before that time.

How long do I have to file a claim on my hail insurance?

If you notice your crop has been hit by a hailstorm, you have 72 hours to complete a “Notice of Loss” form and have that submitted via mail, fax, email or online. The Notice of Loss form is attached with every policy when they are issued. You cannot file a claim over the phone as the insurance company must have a completed Notice of Loss form before adjustment can proceed. If you need help filling out this form or submitting it; we would love to help you out.

If you are busy harvesting when this hailstorm hits, it is important to understand the protocol on adjusting crops that need to be harvested.

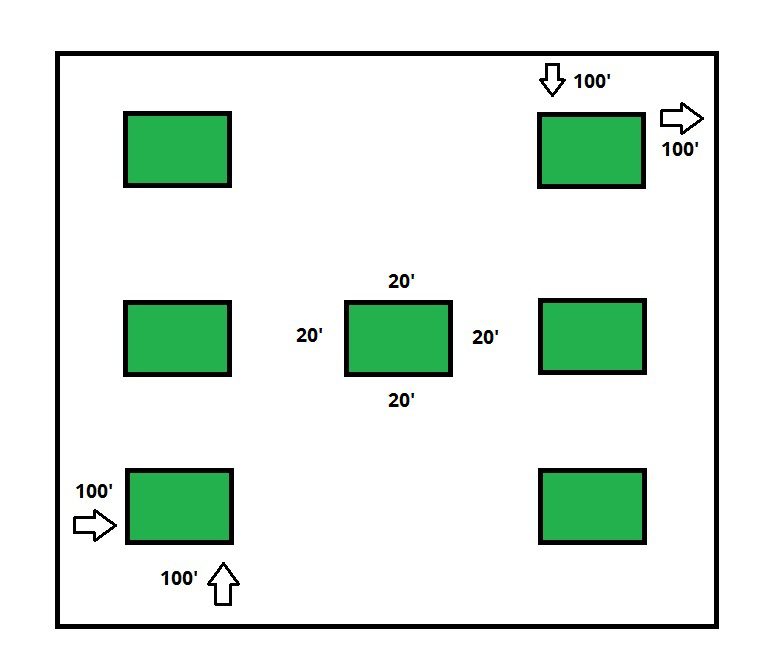

- Where the crop is being turned under, cut for feed or straight combined; leave standing and undisturbed 20×20 foot strips, 100 feet in from the outside edge of the field in each corner.

- If the crop is ready for swathing, leave no crop standing. Swath it all down as the adjuster will do his adjustment from the swath. ***EXCEPTION: Leave standing

- Where the swathed crop is being harvested, leave an undisturbed 30-40 foot strip of swath, 100 feet or at least 3 rows in, from the edge of the field in each corner. For fields in excess of 80 acres leave an additional three strips down the centre of the field. Diagram below.

If a hail claim has been filed and sufficient undisturbed evidence of the crop has not been left for inspection, the question of liability is decided by the insurance company at head office.

What if I cannot afford the premium for full coverage?

There are a number of ways to bring your costs down when insuring against hail damage. You can put a deductible on your policy. We recommend placing a smaller policy with full coverage ($100/acre) and then having a second policy on the same crop with a 20D deductible to reduce premium but provide value if you have a total loss or a large percentage of loss. For more information on deductibles, please contact our office.

You can also defer payment until October 1st if that would be beneficial. There is a 5% finance fee. But this way you can make payment at a later date. We also recommend purchasing on your credit card, as this will buy you some time based on when your monthly credit card payments come due.

There are many variables when purchasing your hail insurance. Come and get a quote from our offices to see how we can insure your land against a potential disaster. It is important to understand how a claim works and what is your responsibility when a hailstorm comes around. If you need more information about this process, please contact our office. That being said, good luck! We hope you have a successful year!